For Vets Seeking Home Loans, the Covid-19 Economy is Making It Harder

Written by:

Patrick Boyaggi

Patrick Boyaggi

CEO an Co-Founder

Patrick is the Co-Founder and CEO of Own Up. He has a wealth of experience and knowledge as a mortgage executive.

See full bio

This article was originally published at MilitaryTimes.com on April 28, 2020.

A home is typically a person’s largest and most important asset. Therefore, whether you’re buying a house for the first time or you’re refinancing into a lower rate mortgage, it’s imperative that you don’t overpay.

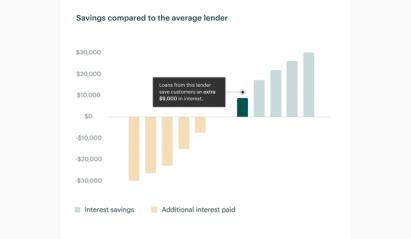

Shopping for a mortgage is important because interest rates can vary between lenders by as much as 1 percent, and in some cases, the interest rates offered to you by the same lender can vary, depending on the loan originator’s commission. This is true of all home loans, including those insured by the Department of Veteran Affairs. This means that failing to shop for a mortgage can cost you thousands of dollars in upfront costs and tens of thousands in excess interest over the life of your loan.

While it’s important for veterans to shop for a mortgage in all economic environments, it’s especially important to do so during the current economic crisis caused by COVID-19. The reason? Capital is being reserved for loans to borrowers who are perceived to be the lowest risk (i.e. prime loans which are made to borrowers with high credit scores, low debt-to-income ratios, and higher down payments). This “flight to safety,” which is perpetuated by the uncertainty about the future of the economy, is causing an increase in interest rates for loans insured by government loans like those from the Department of Veterans Affairs and the Federal Housing Administration because these loans are perceived to be higher risk. Therefore, despite the Federal Reserve’s commitment to buy trillions of dollars of mortgage-backed securities, lenders that originate the loans that ultimately go into these securities are tightening their credit standards, raising interest rates to offset risk, and in some cases, even suspending government loan products all together.

For example, today a borrower with a 740-plus credit and 20 percent down that is securing conventional financing can expect interest rates near historic lows. On the other hand, a borrower with a credit score below 640 and less than 20 percent down can expect interest rates a full 1 percent to 2 percent higher than what was available just several weeks ago, if financing is even available at all. The spread between interest rates offered by lenders for conforming loans and government loans has widened because the investors that buy the mortgage-backed securities made up of government loans are demanding abnormally high returns for the additional risk.

Not only is shopping for a mortgage important to ensure you don’t overpay, but it can be the difference between securing financing or getting denied. In fact, at my company, Own Up, a veteran that recently used our service to shop for a mortgage was able to find a lender in our marketplace that offered an interest rate 0.75 percent below what he was being offered from his existing lender. This experience will save him and his family more than $17,000 over the life of the loan.

Own Up can shop a marketplace of lenders to get you customized refinance and purchase offers without a hard credit check – click here to take a short questionnaire and get started.

All mortgage lenders are under pressure due to the current economic crisis, and that is affecting rates for all government loans, including VA loans. However, there are still many lenders out there that are willing to work with veterans and will do their very best to make sure you’re getting fair terms. In times like these, it’s important for everyone to look for ways to save money, and there is no better place to start than with your home mortgage.

Our mission is to empower Americans with personalized data and unbiased advice so they can make better financial decisions. Personal finances are personal – a complex web of factors made all the more complicated when economic uncertainty strikes. We're here to answer questions and provide guidance. Email us at hello@ownup.com.